Loan on Floating Interest Rate and Fixed Interest Rate Difference

When it comes to borrowing money—whether for a home, car, or personal needs—understanding the type of interest rate attached to your loan is crucial. Two of the most common types are fixed interest rate and floating interest rate. Each has its advantages and disadvantages, and the best choice depends on your financial goals, market conditions, and risk tolerance.

In this blog post, we’ll explore the key differences between floating and fixed interest rate loans, explain how they work, and help you decide which one might be right for you.

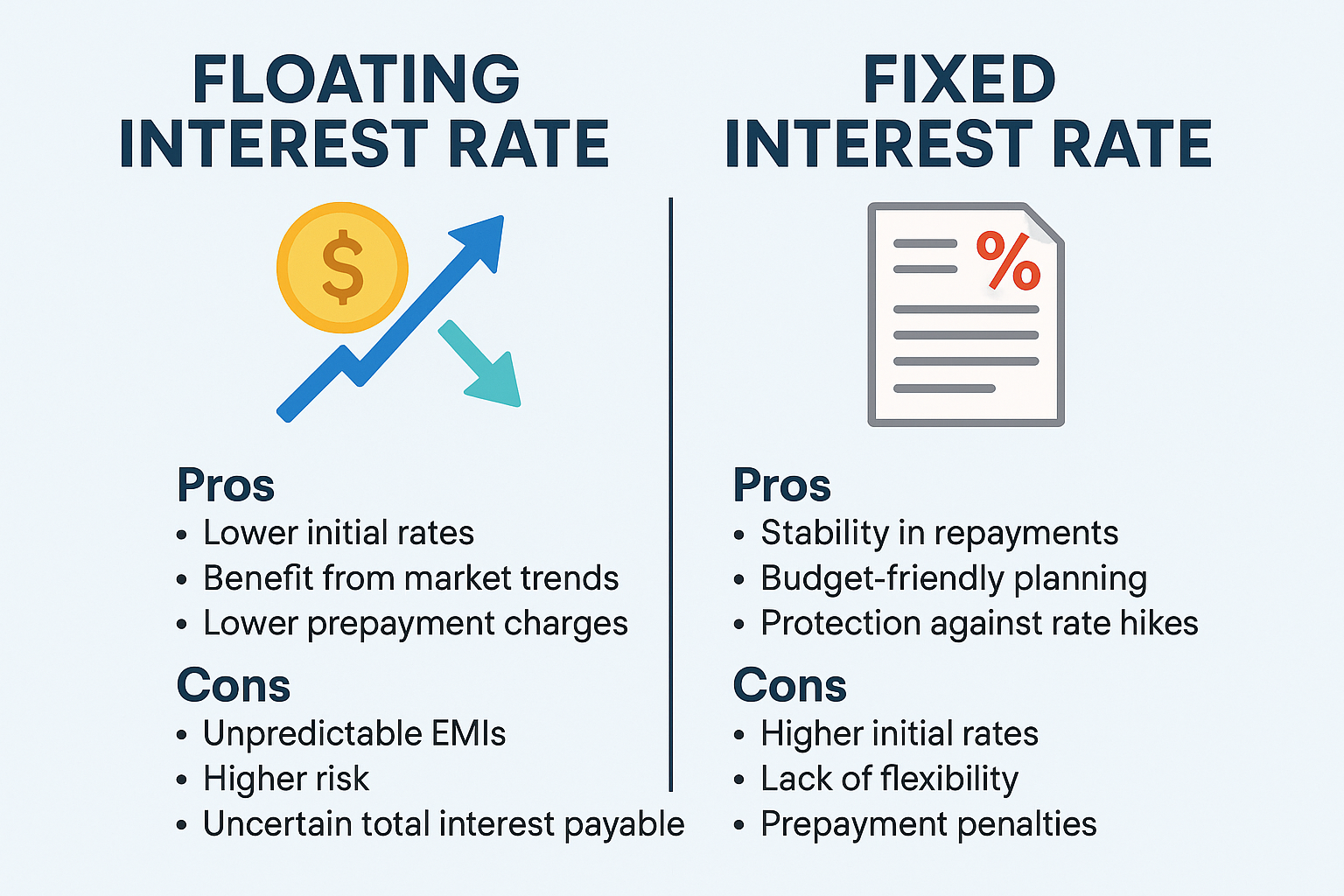

What is a Fixed Interest Rate?

A fixed interest rate remains constant for the entire tenure of the loan. Whether the market interest rates rise or fall, your interest rate and EMI (Equated Monthly Installment) remain the same.

✔️ Key Features of Fixed Interest Rate Loans:

-

Interest rate is locked at the time of loan approval.

-

Monthly payments remain predictable.

-

Not affected by market fluctuations.

Post Comment Cancel reply